When it comes to the US economy today, what you see depends on where you look. Business sentiment indicators suggest recession is imminent, while consumers seem to have a much sunnier outlook. What’s all this telling us?

To start with, this confirms that the economic recovery from the COVID-19 pandemic has been unique by any measure. Historical relationships between economic variables simply haven’t been a reliable gauge during this unprecedented period. Not surprisingly, forecasters who rely more on business-based indicators expect an imminent recession, while those more focused on consumer-based indicators, including the Federal Reserve, expect a soft landing.

Our forecast falls somewhere in between. We believe that the supply and demand sides of the economy meet at the labor market. And it, though strong by historical standards, has started to soften. That is likely to continue, in our view, which suggests we’ll see the broader economy slow in the months ahead. Whether it falls into recession or not remains a close call; if it does, the recession is likely to be a mild one.

A Tale of Two Outlooks

There is little doubt that businesses are skeptical of the forward outlook for the economy. The most reliable indicator of how businesses perceive the environment is the Institute for Supply Management (ISM) manufacturing survey. While the index hasn’t hit recessionary levels yet, it is headed in that direction (Display).

Banks, too, see a deteriorating environment. Lending standards have tightened, as they typically do when the economy approaches a downturn. Even more interestingly, however, banks have reported a large decline in demand for loans from businesses of all sizes. That decline suggests quite strongly that businesses are not looking to expand into what they perceive to be a deteriorating economy

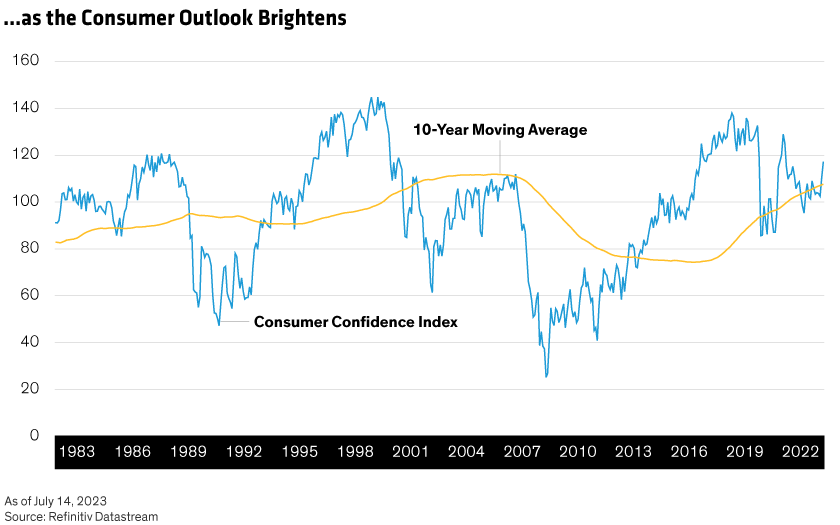

Consumers, on the other hand, seem to be living in an entirely different economy. While business sentiment has declined, consumer confidence has surged higher in recent months and is now above its long-term average (Display).

Why the bounce? We think it has much to do with disinflation. Yes, inflation remains well above the normal levels that have prevailed over the long term. But headline inflation, which includes energy costs, has slowed from a growth rate of more than 6% at the beginning of the year to roughly 3% today. That has helped household income go further and boosted overall confidence.

Will this continue? Yes and no.

Let’s start with the affirmative. We expect to see some additional disinflation and anticipate that the Fed will hit its 2% inflation target sometime in 2024. But keep in mind that inflation has fallen by more than 3% over the past six months. An additional 1% slide over the next 18 months is unlikely to provide the same sort of boost in consumer confidence.

Then there’s the labor market. We expect to see some slowdown there, too. Wage growth has already fallen by about 1.5 percentage points this year—about half the amount by which inflation has slowed—and we think there may be further decline. As inflation comes down, firms will feel less pressure to raise wages.

In addition to slowing wage growth, we have started to see broader signs of labor market cooling. The number of open jobs has started to decline, and the rate of hiring has fallen over the course of the year.

To be clear, the labor market is still strong. While there are signs that it is easing somewhat, there is still a long way to go. So even though we expect the process to continue, we don’t expect consumer sentiment to plumb the depths to which corporate sentiment has fallen.

Instead, we expect the two readings to meet somewhere in the middle. Businesses will be buoyed by consumer spending in the coming months, which should boost their perception of the economy. And households will likely perceive a bit of weakening in their situation as the labor market cools. That combination suggests to us that rather than focusing too intently on one or the other, the best way to view the path forward is to split the difference: things aren’t as bad as businesses perceive them to be, nor are they as rosy as households seem to think.

When it comes to our forecast, this all adds up to GDP growth that will be positive, but below trend, for the next 18 months.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.