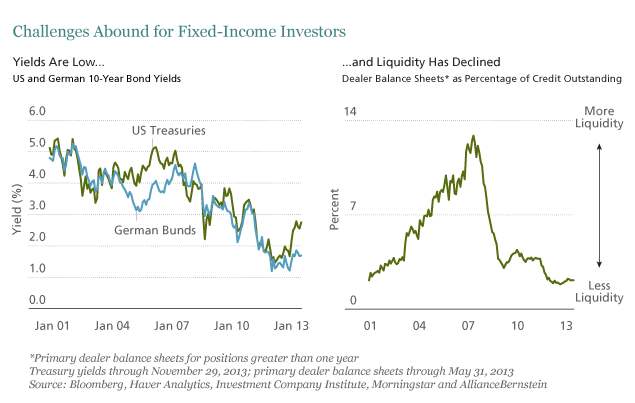

After a 30-year bull run in bond markets, fixed-income investors are finding that their ability to maintain alpha is becoming increasingly challenged. For example, nominal yields are low and market liquidity has declined (Display)—conditions which, respectively, lower the dispersion of returns (and so limit the opportunities for investment) and put upward pressure on transaction costs.

For many investors, this adds up to a bleak prospect of diminishing returns and sources of alpha.

We do not accept that such an outcome is inevitable, however. In our view, investors stand a very good chance of maintaining, and perhaps even improving, alpha if they are willing to explore new ways to capture it.

The way to preserve or improve alpha and risk-adjusted returns in this environment, in our view, lies not just in capturing upside, but also in limiting the potential downside of an investment opportunity. Such an approach consists of generating asymmetric returns, or what the fixed-income world calls positive convexity.

The big question, of course, is: how can investors achieve such results? In this paper, we attempt to answer this question by looking at some of the enhanced investment techniques that can generate alpha with asymmetric return profiles.